The Two Capitalisms: Electric Batteries as a Case Study in US Magical Thinking vs. Chinese Vertical Integration

By Jack Lifton, a consultant, author, and lecturer on the market fundamentals of the technology metals

Capitalism with Chinese Characteristics, (CWCC) as the Chinese press officially refers to the use of capitalism by the Chinese Communist Party (CCP) to advance socialism in China, is winning the battle with the neoliberal, “free and efficient,” market that supposedly has led the USA, first and foremost, to “the end of history.” CWCC has transferred enough wealth from the west to the east to ignite self-sustaining growth in China’s GDP.

Our world dominated by two capitalisms; the “free market” variety practiced in one form or another by almost all of the industrialized countries except Russia and a few others with a strong authoritarian bent; and “Capitalism with Chinese Characteristics (their official description) practiced of course by the Peoples’ Republic of China.

Let’s look at how the two capitalisms have fared in creating a secure supply of the raw materials for manufacturing energy storage and production devices for the storage of and production of alternate (to fossil fuel produced) energy. Access to supplies is critical to prevent shortages and to help assure market position.

Notwithstanding the illogical blather about globalization, its purpose outside of China in the last generation has been to enrich a small segment of western society without regard to the welfare of the general populations in those countries. Natural resource imperialism has been the driver of globalization for centuries. But the countries that were once victims of resource imperialism are in the process of turning the tables via total vertical integration of the production, use, and marketing of consumer goods critically enabled by those natural resources.

Specifically, the overarching purpose of Chinese business is to achieve Chinese independence of global markets for the basic needs of a widespread technological society second to none.

The Chinese focused first on the security of a growing Chinese INDUSTRIAL economy by seeking to attain natural resource total supply chain self-sufficiency. The country is now addressing health and safety.

Chinese politicians pursue national objectives through a reestablished mandarinate, a reproduction in part of their own ancient approach to large scale governance by a meritocratically selected and educated elite. They have dded to that a bit of the ancient Roman cursus honorum, the path that a member of the ruling class must take in order to advance to senior roles in their one party government. No Justin Trudeau’s; Eduard Macron’ or even Donald Trump can take power in their system. It does help to be directly descended from a founder of the Chinese Communist Party or its hierarchy but experience in government, and a specialized education, is an absolute requirement for the top job(s) in today’s China.

By contrast, American politicians; public intellectuals; and opinion makers are committed to magical thinking; they hold that beliefs are more important than mere facts. When they recognize a “crisis,” which they define as “when things aren’t going the way they are supposed to go to keep us personally wealthy and powerful indefinitely” their response is to first “study” the problem (to get it out of the public eye) and then after consultation with each other throw money at “solutions” that have been proposed by properly credentialed “experts’ and others who are the “right sort (their class) of people.” Thus we get neoliberal economics with its conceit that a “free” market will always be both efficient and “ultimately” keep supply and demand in balance through directing capital to where it is needed to do so.

The FACT; it is not a belief or conjecture; but an obvious fact that a consumer society built upon technology is completely dependent upon the production of just a few key materials derived from natural resources. This is well understood by the Chinese mandarinate, and since the goal of the CCP is to build such a society, it has resulted in a national mandate for China to become self-sufficient in these key materials for technology as soon as possible. The Chinese are not natural resource globalists; in fact they are natural resource imperialists for want of a better term.

As Mao Zedong said when the Chinese communist takeover was floundering economically, “Let a thousand flowers bloom,” i.e. try everything

His brilliant successor, Deng Xiaoping, decreed that China must quietly become wealthy and powerful, and for this he allowed the first use of capitalism to advance those goals through selecting the best results of letting a thousand flowers bloom.

Today’s Chinese leaders, less charismatic but dedicated to the same goals, have promulgated a modified capitalism (with Chinese characteristics) to achieve self-sufficiency in production and then supply of goods determined to be critical to the future of Chinese society.

And now they are sorting out the various approached to capitalism and the selected target resources to make CWCC as efficient as possible to achieve the goals that have been so identified.

The mandarins convinced Deng that China’s abundance of rare earths was important, because they foresaw that the miniaturization of electronic and electrical devices, the main use of rare earths properties, conserved and extended commodity natural resources such as iron, steel, aluminum, copper, and fossil fuels, thus advancing China’s goal of self-sufficiency. Within one generation the Chinese rare earth supply chain had become vertically integrated and was a global monopoly; this was mostly achieved because China’s construction of a total downstream (from mining and refining) supply chain allowed it also to become a monopsony in the final assembly of goods dependent for their operations upon the electronic properties of the rare earths. This monopoly/monopsony was the intended goal!

Of particular interest today is that China’s rulers have now determined that they must electrify personal as well as mass transportation on the ground in order to eliminate an unforeseen (by them) problem: massive air pollution in their mega cities caused by the concentrations there of fossil-fueled vehicles (which in the general scheme of things globally produce only two percent of “pollution,” but their concentrations in cities are principal contributors to it in those locales).

China’s “President” mandated first that China’s 90 motor vehicle assemblers and 40 lithium ion battery manufacturers produce 5,000,00 electrified (mainly battery powered) motor vehicles by 2020. Then they extended the “mandate” to foreign automakers manufacturing or selling cars in China, and furthermore, required that only Chinese manufactured batteries may be used in motor vehicles made or sold in China!!

The Chinese domestic battery maker’s very first response was that they did not have the manufacturing capacity nor access to the raw materials necessary. The response of the long term goal directed CCC was to use CWCC to “encourage” Chinese mining, refining, and fabricating industries (dominated by SOES) to develop or purchase the critical natural resources and to expand their capacities to meet the needs of the mandate. The Bank of China was ordered to “facilitate” such investments GLOBALLY-but and this cannot be overemphasized-globalization of sourcing for the PROC means the acquisition globally for use IN CHINA of natural resources! It does not mean acquiring foreign sources of natural resources to produce them as raw materials for global markets, NOT AT ALL!

By contrast, free market capitalism has today been almost totally financialized. Its purpose has become the transfer of money to a few, not the creation of new wealth in the financier’s home country through building factories and creating jobs. In fact, the moneyed elites have become what the Soviets used to call “cosmopolitans,” which were the criminals who put self before cause or country. Although it is easier for a Chinese national to “escape’ than it ever was for a Soviet citizen, it is still a crime in China to make or sequester money that is not for the purpose of advancing China’s path to socialism. Expatriates are shunned if they try to return and the amount of capital that can be exported from China for personal use is strictly limited.

With that introduction, let me now look at the influence on world commodity markets of the Chinese goal of the electrification of motor vehicles for personal use. The issues in the west have been driving range and the selling price of the vehicles.

The nebulous goal in the USA is allegedly to save the planet. In China, it is to immediately reduce pollution in the cities. American free market capitalism wants a relatively short term return on capital. CWCCs wants a self sufficient Chinese economy with return on capital to be measured by including the success of the Chinese standard of living and quality of life.

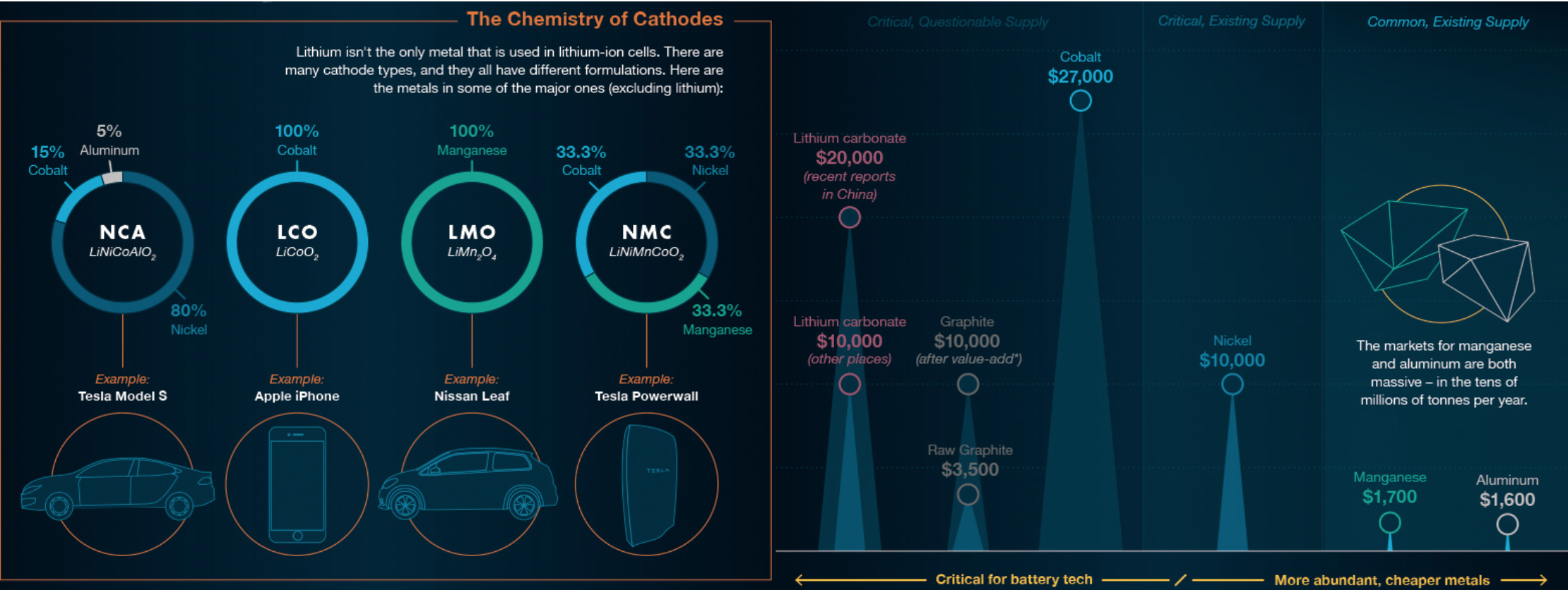

Let’s look at the critical natural resources necessary for producing lithium ion batteries that can give a one to two ton motor vehicle a range of 300 km or more; these would be of the of the NCA, nickel-cobalt-aluminum cathode type such as is used by the Tesla corporation.

Note that the above comparative chart shows that the Tesla Model 3 battery contains only half as much cobalt as the Tesla Powerwall home power battery, for which the Tesla organization projects an even larger market than that for motor vehicles.

Note also that the chart does not state how much lithium would be used in these batteries. For the Model 3 unit that number would be 10 kg, calculated as lithium metal, or 60 kg calculated as the more common commodity unit for lithium, which is lithium carbonate. Neither copper (more than 75 kg), which is not even mentioned, nor aluminum (6 kg) are listed as “critical.” I think that this is because the chart’s author knows that both metals are produced annually in the 10s of millions of tons; 25 in the case of copper, and 50 in the case of aluminum (Note at this point and keep it in mind that China uses and refines from ore concentrates, intermediate forms; and scrap ONE-HALF of all of both the aluminum and the copper used on this planet annually!

As the chart shows there would be 19 kg of cobalt (measured as metal) and 100 kg of nickel, measured as metal in a Model S battery, which weighs around 500 kg in total when assembled.

Let’s see how much of each metal would be used to manufacture batteries for 500,000 2018 Tesla Model 3s.

Note that the above comparative chart shows that the Tesla Model 3 battery contains only half as much cobalt as the Tesla Powerwall home power battery, for which the Tesla organization projects an even larger market than that for motor vehicles.

Note also that the chart does not state how much lithium would be used in these batteries. For the Model 3 unit that number would be 10 kg, calculated as lithium metal, or 60 kg calculated as the more common commodity unit for lithium, which is lithium carbonate. Neither copper (more than 75 kg), which is not even mentioned, nor aluminum (6 kg) are listed as “critical.” I think that this is because the chart’s author knows that both metals are produced annually in the 10s of millions of tons; 25 in the case of copper, and 50 in the case of aluminum (Note at this point and keep it in mind that China uses and refines from ore concentrates, intermediate forms; and scrap ONE-HALF of all of both the aluminum and the copper used on this planet annually!

As the chart shows there would be 19 kg of cobalt (measured as metal) and 100 kg of nickel, measured as metal in a Model S battery, which weighs around 500 kg in total when assembled.

Let’s see how much of each metal would be used to manufacture batteries for 500,000 2018 Tesla Model 3s.

Cobalt: 19 kg/battery x 500,000 batteries = 9,500 metric tons of cobalt

Lithium: 10 kg/battery x 500,000 batteries = 5,000 metric tons of lithium

Nickel: 100 kg/battery x 500,000 batteries = 50,000 metric tons of nickel

Copper: 75 kg/battery x 500,000 batteries = 37,500 metric tons of copper

Now let’s look at the USGS estimate for the total production of each of the above metals in 2016

Cobalt = 123,000 metric tons

Lithium = 35,000 metric tons

Nickel = 2,250,000 metric tons

Copper = 19,400,000 metric tons

Therefore the 2018 production run of the Tesla Model 3 will require:

13% of the world’s new production of COBALT

14% of the world’s new production of LITHIUM

2.3% of the world’s new production of NICKEL

2% of the world’s new production of COPPER

Now let’s look at where the above metals are refined into ready for use lithium ion battery grade forms. Actually let’s just look at what percentage of all of the above metals are so refined in the PRC:

Cobalt = 60%

Lithium = 50+%

Nickel = 52%

Copper = 40%

But there’s a problem. As I have stated the Chinese do not like to export raw materials; they prefer finished goods containing those raw materials, so that when they do export finished goods (in excess of their domestic needs) they capture all of the value added prior to direct marketing. The overwhelming proportion of lithium ion battery makers are domestic Chinese firms or Chinese dominated ventures with Japanese or Korean firms. Therefore the Chinese market has a monopsony on lithium ion batteries for use in ground transportation.

As an aside at this point I note that according to the USGS the United States imported 11,000 tons of cobalt in 2016. This means that Tesla’s needs alone would essentially double the amount of cobalt imported into the USA by the end of 2018. This would have to be battery grade cobalt produced outside of China, and since the amount of new cobalt produced annually in the US is negligible and China refines 60% of the world’s cobalt, it would mean that the US would require nearly half of the new cobalt produced and refined outside of China in 2018 unless Chinese made batteries are counted as cobalt imports.

Is it possible that Tesla alone could use as much cobalt as the rest of the United States industry altogether? Yes, it is. But is it likely? No, it isn’t. Remember that these demand figures do not take into account any Powerwall Battery production, or the substantial contract Tesla announced in Australia to install a huge Powerwall facility there.

I also note in passing that the USA does not have sufficient domestic lithium refining capacity, not to mention mining capacity to deliver to Tesla 14% of next year’s total global lithium production. And China is well on the way to monopsonizing global lithium use for electrified motor vehicles’ batteries.

At this point, we need to revisit China’s mandate to produce domestically 5,000,000 electrified motor vehicles by the end of 2020. If these vehicles used the same type of battery as Tesla’s Model 3 to achieve a range on a charge equal to that of a medium size fossil fueled vehicle,1 then the Chinese OEM electrified vehicle industry would require essentially all of the 2020 new production of cobalt and lithium under any possible scenario of increases in the new production of either metal. It would also require a substantial increase in Chinese refining and fabrication capacity for battery grades and forms of the two metals. Is that possible? Yes. Is it likely? No, because it would completely disrupt the world’s supply and value chains for cobalt and lithium.

Of course China could opt for a majority of the mandated production to be of shorter range EVs for city driving. I think this is in fact likely.

But China has mandated that by 2030 30% of all cars manufactured in China must be EVs. Based on today’s 25 million units per year (the world’s largest production in one nation) this would be 7.5 million EVs per year, a figure which would have been reached by building on 2020’s 5 million units! This would mean an average production of 6 million units per year, so that by 2030 China would have manufactured 60 million EVs!! The modern lithium ion batteries for long range use are intended to last up to 10 years, so that the Chinese production alone would tie up (immobilize and therefore be unavailable for recycling) several years of global new production of cobalt and lithium and impact even the global supply of nickel and copper.

In the USA and Europe range is more important than in China, so the projections of increased penetration of those markets by long range EVs, such as the Tesla, should add just as much demand in those two markets combined as in China.

Short sighted speculators will try and corner the cobalt and lithium markets surely. Realizing this is one reason that Chinese companies are acquiring cobalt, nickel, and copper properties and mines aggressively right now. The Chinese government is very much encouraging this.

I suspect that long range EVs using cobalt based cathode technogies will ultimately be the status symbols of the wealthy, and that the world’s EV fleet will be powered by shorter range power trains using more available cathode materials.

This scenario will allow cobalt prices to increase to where they would have to be for free market capitalism to “invest.’ In the meantime capitalism with Chinese characteristics has basically won the race to be the first to mass produce a mix of city and country (longer range) EV’s that are affordable in their markets. I suspect that Chinese car and battery makers are already planning sufficient production so as to be able to export “surplus’ EVs of both types to the US, European, Asian, and African markets by 2020.

The best way to invest in the projected EV market boom is to invest in producers, refiners, fabricators and recyclers of the cathode materials for lithium ion batteries for motor vehicle and stationary power use. Stay away from the non-Asian car makers; they have not understood critical raw material constraints and that misunderstanding is about to bite them in the tailpipe.

Norway, the UK, and Germany can ban fossil fueled cars by 2040, but by the numbers it will be the Chinese car industry that benefits most from this move.

Don’t say I didn’t tell you so.

____

1 In an earlier post on the importance of cobalt to the production of electric vehicle batteries, some readers objected by saying that other battery technologies that did not use cobalt were close enough to be commercialized so as to make this concern moot in a few years.

The problem with this reasoning is that the automotive industry has long production lead times. And at least as important, the OEM automotive industry investment in innovation is subject to the herd mentality. No where is this more true than in “advanced” anything (here read “battery”) technology.”

The global OEM automotive industry was very little investment (or interest) in proulsion battery research prior to the 21st century. EVs like flying cars, were viewed as marginal and niche markets at best. Then, as always, a “major” stepped into the water about 25 years ago. Toyota took an idea pioneered by (the soon then to be defunct) International Harvester personal vehicle manufacturing division (anyone remember the Harvester “Scout?”) called the “hybrid” power train and created the Toyota Prius NOT TO MAKE THE WORLD GREENER OR TO REDUCE THE IMPACT OF (THEN CONSIDERED HARMLESS) MAN MADE CARBON DIOXIDE, but to meet California’s then requirement of 2% zero TOXIC emission vehicles in a company’s product line.

Noting that GM’s EV1 was going to be (and was) an economic flop, and considering that failure to be due in part to the weight, maintenance required, hazard of fire(!), short cycle life, and power disadvantages of lead acid batteries, adopted a then “new” technology known as the nickel metal (rare earths) hydride battery, which ameliorated the dangers of lead-acid and even though it cost more to build, it added 50% to the RANGE!

Fickle, perhaps bribed, California politicians rescinded the zero emissions mandate at the last minute and GM scrapped the EV1 program as fast as it could.

But Toyota felt that its approach has created a “new” product, so it introduced the Prius into the Japanese market in 1997, where it became a success and is still in the product line today, 20 years later.

Fifteen years after introducing the Prius, Toyota began selling a plug-in version using a lithium ion battery. The company today still offers the nickel metal hydride version of the Prius, but has announced phasing it out in favor of the lithium ion battery. Total product cycle time expended since the Prius was first engineered has been TWENTY FIVE YEARS. Note that only Toyota has had this profitable result with nickel metal hydride batteries. GM introduced a hybrid Buick in 2008 using nickel metal hydride technology, and all 8,000 units had mechanical battery failures! Ford waited longer and went immediately (after 3 years of production part approval process, PPAP) to a lithium ion battery.

Disruptive some technologies may be, but their adoption by manufacturers of civilian goods is at the margins, and profitability and product differentiation are the drivers NOT JUST INNOVATION.

Globally, after ONLY 10 years of study, OEM car makers have chosen cobalt using cathode chemistries requiring liquid electrolytes and graphite anodes for long range electric power trains. Toyota is once again an outlier looking at solid state electrolyte lithium ion batteries. In 25 years or so this technology, or that of fuel cells (solid state but not using platinum group metals or scandium, neither of which are abundant enough) may displace liquid electrolyte cells. But then again they may not, even if they work and work well scale up may not be possible due to critical material constraints or mechanical or electronic issues. It’s a crap shoot and magical thinking about moving innovation from the bench top to the showroom disruptively and immediately won’t help.

By Jack Lifton, a consultant, author, and lecturer on the market fundamentals of the technology metals

Capitalism with Chinese Characteristics, (CWCC) as the Chinese press officially refers to the use of capitalism by the Chinese Communist Party (CCP) to advance socialism in China, is winning the battle with the neoliberal, “free and efficient,” market that supposedly has led the USA, first and foremost, to “the end of history.” CWCC has transferred enough wealth from the west to the east to ignite self-sustaining growth in China’s GDP.

Our world dominated by two capitalisms; the “free market” variety practiced in one form or another by almost all of the industrialized countries except Russia and a few others with a strong authoritarian bent; and “Capitalism with Chinese Characteristics (their official description) practiced of course by the Peoples’ Republic of China.

Let’s look at how the two capitalisms have fared in creating a secure supply of the raw materials for manufacturing energy storage and production devices for the storage of and production of alternate (to fossil fuel produced) energy. Access to supplies is critical to prevent shortages and to help assure market position.

Notwithstanding the illogical blather about globalization, its purpose outside of China in the last generation has been to enrich a small segment of western society without regard to the welfare of the general populations in those countries. Natural resource imperialism has been the driver of globalization for centuries. But the countries that were once victims of resource imperialism are in the process of turning the tables via total vertical integration of the production, use, and marketing of consumer goods critically enabled by those natural resources.

Specifically, the overarching purpose of Chinese business is to achieve Chinese independence of global markets for the basic needs of a widespread technological society second to none.

The Chinese focused first on the security of a growing Chinese INDUSTRIAL economy by seeking to attain natural resource total supply chain self-sufficiency. The country is now addressing health and safety.

Chinese politicians pursue national objectives through a reestablished mandarinate, a reproduction in part of their own ancient approach to large scale governance by a meritocratically selected and educated elite. They have dded to that a bit of the ancient Roman cursus honorum, the path that a member of the ruling class must take in order to advance to senior roles in their one party government. No Justin Trudeau’s; Eduard Macron’ or even Donald Trump can take power in their system. It does help to be directly descended from a founder of the Chinese Communist Party or its hierarchy but experience in government, and a specialized education, is an absolute requirement for the top job(s) in today’s China.

By contrast, American politicians; public intellectuals; and opinion makers are committed to magical thinking; they hold that beliefs are more important than mere facts. When they recognize a “crisis,” which they define as “when things aren’t going the way they are supposed to go to keep us personally wealthy and powerful indefinitely” their response is to first “study” the problem (to get it out of the public eye) and then after consultation with each other throw money at “solutions” that have been proposed by properly credentialed “experts’ and others who are the “right sort (their class) of people.” Thus we get neoliberal economics with its conceit that a “free” market will always be both efficient and “ultimately” keep supply and demand in balance through directing capital to where it is needed to do so.

The FACT; it is not a belief or conjecture; but an obvious fact that a consumer society built upon technology is completely dependent upon the production of just a few key materials derived from natural resources. This is well understood by the Chinese mandarinate, and since the goal of the CCP is to build such a society, it has resulted in a national mandate for China to become self-sufficient in these key materials for technology as soon as possible. The Chinese are not natural resource globalists; in fact they are natural resource imperialists for want of a better term.

As Mao Zedong said when the Chinese communist takeover was floundering economically, “Let a thousand flowers bloom,” i.e. try everything

His brilliant successor, Deng Xiaoping, decreed that China must quietly become wealthy and powerful, and for this he allowed the first use of capitalism to advance those goals through selecting the best results of letting a thousand flowers bloom.

Today’s Chinese leaders, less charismatic but dedicated to the same goals, have promulgated a modified capitalism (with Chinese characteristics) to achieve self-sufficiency in production and then supply of goods determined to be critical to the future of Chinese society.

And now they are sorting out the various approached to capitalism and the selected target resources to make CWCC as efficient as possible to achieve the goals that have been so identified.

The mandarins convinced Deng that China’s abundance of rare earths was important, because they foresaw that the miniaturization of electronic and electrical devices, the main use of rare earths properties, conserved and extended commodity natural resources such as iron, steel, aluminum, copper, and fossil fuels, thus advancing China’s goal of self-sufficiency. Within one generation the Chinese rare earth supply chain had become vertically integrated and was a global monopoly; this was mostly achieved because China’s construction of a total downstream (from mining and refining) supply chain allowed it also to become a monopsony in the final assembly of goods dependent for their operations upon the electronic properties of the rare earths. This monopoly/monopsony was the intended goal!

Of particular interest today is that China’s rulers have now determined that they must electrify personal as well as mass transportation on the ground in order to eliminate an unforeseen (by them) problem: massive air pollution in their mega cities caused by the concentrations there of fossil-fueled vehicles (which in the general scheme of things globally produce only two percent of “pollution,” but their concentrations in cities are principal contributors to it in those locales).

China’s “President” mandated first that China’s 90 motor vehicle assemblers and 40 lithium ion battery manufacturers produce 5,000,00 electrified (mainly battery powered) motor vehicles by 2020. Then they extended the “mandate” to foreign automakers manufacturing or selling cars in China, and furthermore, required that only Chinese manufactured batteries may be used in motor vehicles made or sold in China!!

The Chinese domestic battery maker’s very first response was that they did not have the manufacturing capacity nor access to the raw materials necessary. The response of the long term goal directed CCC was to use CWCC to “encourage” Chinese mining, refining, and fabricating industries (dominated by SOES) to develop or purchase the critical natural resources and to expand their capacities to meet the needs of the mandate. The Bank of China was ordered to “facilitate” such investments GLOBALLY-but and this cannot be overemphasized-globalization of sourcing for the PROC means the acquisition globally for use IN CHINA of natural resources! It does not mean acquiring foreign sources of natural resources to produce them as raw materials for global markets, NOT AT ALL!

By contrast, free market capitalism has today been almost totally financialized. Its purpose has become the transfer of money to a few, not the creation of new wealth in the financier’s home country through building factories and creating jobs. In fact, the moneyed elites have become what the Soviets used to call “cosmopolitans,” which were the criminals who put self before cause or country. Although it is easier for a Chinese national to “escape’ than it ever was for a Soviet citizen, it is still a crime in China to make or sequester money that is not for the purpose of advancing China’s path to socialism. Expatriates are shunned if they try to return and the amount of capital that can be exported from China for personal use is strictly limited.

With that introduction, let me now look at the influence on world commodity markets of the Chinese goal of the electrification of motor vehicles for personal use. The issues in the west have been driving range and the selling price of the vehicles.

The nebulous goal in the USA is allegedly to save the planet. In China, it is to immediately reduce pollution in the cities. American free market capitalism wants a relatively short term return on capital. CWCCs wants a self sufficient Chinese economy with return on capital to be measured by including the success of the Chinese standard of living and quality of life.

Let’s look at the critical natural resources necessary for producing lithium ion batteries that can give a one to two ton motor vehicle a range of 300 km or more; these would be of the of the NCA, nickel-cobalt-aluminum cathode type such as is used by the Tesla corporation.

Note that the above comparative chart shows that the Tesla Model 3 battery contains only half as much cobalt as the Tesla Powerwall home power battery, for which the Tesla organization projects an even larger market than that for motor vehicles.

Note also that the chart does not state how much lithium would be used in these batteries. For the Model 3 unit that number would be 10 kg, calculated as lithium metal, or 60 kg calculated as the more common commodity unit for lithium, which is lithium carbonate. Neither copper (more than 75 kg), which is not even mentioned, nor aluminum (6 kg) are listed as “critical.” I think that this is because the chart’s author knows that both metals are produced annually in the 10s of millions of tons; 25 in the case of copper, and 50 in the case of aluminum (Note at this point and keep it in mind that China uses and refines from ore concentrates, intermediate forms; and scrap ONE-HALF of all of both the aluminum and the copper used on this planet annually!

As the chart shows there would be 19 kg of cobalt (measured as metal) and 100 kg of nickel, measured as metal in a Model S battery, which weighs around 500 kg in total when assembled.

Let’s see how much of each metal would be used to manufacture batteries for 500,000 2018 Tesla Model 3s.

Cobalt: 19 kg/battery x 500,000 batteries = 9,500 metric tons of cobaltLithium: 10 kg/battery x 500,000 batteries = 5,000 metric tons of lithiumNickel: 100 kg/battery x 500,000 batteries = 50,000 metric tons of nickelCopper: 75 kg/battery x 500,000 batteries = 37,500 metric tons of copper

Now let’s look at the USGS estimate for the total production of each of the above metals in 2016

Cobalt = 123,000 metric tonsLithium = 35,000 metric tonsNickel = 2,250,000 metric tonsCopper = 19,400,000 metric tons

Therefore the 2018 production run of the Tesla Model 3 will require:

13% of the world’s new production of COBALT14% of the world’s new production of LITHIUM2.3% of the world’s new production of NICKEL2% of the world’s new production of COPPER

Now let’s look at where the above metals are refined into ready for use lithium ion battery grade forms. Actually let’s just look at what percentage of all of the above metals are so refined in the PRC:

Cobalt = 60%Lithium = 50+%Nickel = 52%Copper = 40%

But there’s a problem. As I have stated the Chinese do not like to export raw materials; they prefer finished goods containing those raw materials, so that when they do export finished goods (in excess of their domestic needs) they capture all of the value added prior to direct marketing. The overwhelming proportion of lithium ion battery makers are domestic Chinese firms or Chinese dominated ventures with Japanese or Korean firms. Therefore the Chinese market has a monopsony on lithium ion batteries for use in ground transportation.

As an aside at this point I note that according to the USGS the United States imported 11,000 tons of cobalt in 2016. This means that Tesla’s needs alone would essentially double the amount of cobalt imported into the USA by the end of 2018. This would have to be battery grade cobalt produced outside of China, and since the amount of new cobalt produced annually in the US is negligible and China refines 60% of the world’s cobalt, it would mean that the US would require nearly half of the new cobalt produced and refined outside of China in 2018 unless Chinese made batteries are counted as cobalt imports.

Is it possible that Tesla alone could use as much cobalt as the rest of the United States industry altogether? Yes, it is. But is it likely? No, it isn’t. Remember that these demand figures do not take into account any Powerwall Battery production, or the substantial contract Tesla announced in Australia to install a huge Powerwall facility there.

I also note in passing that the USA does not have sufficient domestic lithium refining capacity, not to mention mining capacity to deliver to Tesla 14% of next year’s total global lithium production. And China is well on the way to monopsonizing global lithium use for electrified motor vehicles’ batteries.

At this point, we need to revisit China’s mandate to produce domestically 5,000,000 electrified motor vehicles by the end of 2020. If these vehicles used the same type of battery as Tesla’s Model 3 to achieve a range on a charge equal to that of a medium size fossil fueled vehicle,1 then the Chinese OEM electrified vehicle industry would require essentially all of the 2020 new production of cobalt and lithium under any possible scenario of increases in the new production of either metal. It would also require a substantial increase in Chinese refining and fabrication capacity for battery grades and forms of the two metals. Is that possible? Yes. Is it likely? No, because it would completely disrupt the world’s supply and value chains for cobalt and lithium.

Of course China could opt for a majority of the mandated production to be of shorter range EVs for city driving. I think this is in fact likely.

But China has mandated that by 2030 30% of all cars manufactured in China must be EVs. Based on today’s 25 million units per year (the world’s largest production in one nation) this would be 7.5 million EVs per year, a figure which would have been reached by building on 2020’s 5 million units! This would mean an average production of 6 million units per year, so that by 2030 China would have manufactured 60 million EVs!! The modern lithium ion batteries for long range use are intended to last up to 10 years, so that the Chinese production alone would tie up (immobilize and therefore be unavailable for recycling) several years of global new production of cobalt and lithium and impact even the global supply of nickel and copper.

In the USA and Europe range is more important than in China, so the projections of increased penetration of those markets by long range EVs, such as the Tesla, should add just as much demand in those two markets combined as in China.

Short sighted speculators will try and corner the cobalt and lithium markets surely. Realizing this is one reason that Chinese companies are acquiring cobalt, nickel, and copper properties and mines aggressively right now. The Chinese government is very much encouraging this.

I suspect that long range EVs using cobalt based cathode technogies will ultimately be the status symbols of the wealthy, and that the world’s EV fleet will be powered by shorter range power trains using more available cathode materials.

This scenario will allow cobalt prices to increase to where they would have to be for free market capitalism to “invest.’ In the meantime capitalism with Chinese characteristics has basically won the race to be the first to mass produce a mix of city and country (longer range) EV’s that are affordable in their markets. I suspect that Chinese car and battery makers are already planning sufficient production so as to be able to export “surplus’ EVs of both types to the US, European, Asian, and African markets by 2020.

The best way to invest in the projected EV market boom is to invest in producers, refiners, fabricators and recyclers of the cathode materials for lithium ion batteries for motor vehicle and stationary power use. Stay away from the non-Asian car makers; they have not understood critical raw material constraints and that misunderstanding is about to bite them in the tailpipe.

Norway, the UK, and Germany can ban fossil fueled cars by 2040, but by the numbers it will be the Chinese car industry that benefits most from this move.

Don’t say I didn’t tell you so.

____

1 In an earlier post on the importance of cobalt to the production of electric vehicle batteries, some readers objected by saying that other battery technologies that did not use cobalt were close enough to be commercialized so as to make this concern moot in a few years.

The problem with this reasoning is that the automotive industry has long production lead times. And at least as important, the OEM automotive industry investment in innovation is subject to the herd mentality. No where is this more true than in “advanced” anything (here read “battery”) technology.”

The global OEM automotive industry was very little investment (or interest) in proulsion battery research prior to the 21st century. EVs like flying cars, were viewed as marginal and niche markets at best. Then, as always, a “major” stepped into the water about 25 years ago. Toyota took an idea pioneered by (the soon then to be defunct) International Harvester personal vehicle manufacturing division (anyone remember the Harvester “Scout?”) called the “hybrid” power train and created the Toyota Prius NOT TO MAKE THE WORLD GREENER OR TO REDUCE THE IMPACT OF (THEN CONSIDERED HARMLESS) MAN MADE CARBON DIOXIDE, but to meet California’s then requirement of 2% zero TOXIC emission vehicles in a company’s product line.

Noting that GM’s EV1 was going to be (and was) an economic flop, and considering that failure to be due in part to the weight, maintenance required, hazard of fire(!), short cycle life, and power disadvantages of lead acid batteries, adopted a then “new” technology known as the nickel metal (rare earths) hydride battery, which ameliorated the dangers of lead-acid and even though it cost more to build, it added 50% to the RANGE!

Fickle, perhaps bribed, California politicians rescinded the zero emissions mandate at the last minute and GM scrapped the EV1 program as fast as it could.

But Toyota felt that its approach has created a “new” product, so it introduced the Prius into the Japanese market in 1997, where it became a success and is still in the product line today, 20 years later.

Fifteen years after introducing the Prius, Toyota began selling a plug-in version using a lithium ion battery. The company today still offers the nickel metal hydride version of the Prius, but has announced phasing it out in favor of the lithium ion battery. Total product cycle time expended since the Prius was first engineered has been TWENTY FIVE YEARS. Note that only Toyota has had this profitable result with nickel metal hydride batteries. GM introduced a hybrid Buick in 2008 using nickel metal hydride technology, and all 8,000 units had mechanical battery failures! Ford waited longer and went immediately (after 3 years of production part approval process, PPAP) to a lithium ion battery.

Disruptive some technologies may be, but their adoption by manufacturers of civilian goods is at the margins, and profitability and product differentiation are the drivers NOT JUST INNOVATION.

Globally, after ONLY 10 years of study, OEM car makers have chosen cobalt using cathode chemistries requiring liquid electrolytes and graphite anodes for long range electric power trains. Toyota is once again an outlier looking at solid state electrolyte lithium ion batteries. In 25 years or so this technology, or that of fuel cells (solid state but not using platinum group metals or scandium, neither of which are abundant enough) may displace liquid electrolyte cells. But then again they may not, even if they work and work well scale up may not be possible due to critical material constraints or mechanical or electronic issues. It’s a crap shoot and magical thinking about moving innovation from the bench top to the showroom disruptively and immediately won’t help.

No comments:

Post a Comment